You may or may not have used PersonalFinanceLab in your classes before. Many teachers know how to take advantage of all its resources, but there are always new schools registered that need a basic tutorial on how to use the platform.

With that in mind, we created this post to highlight the main points you should know about the Budget Game. If you have any further questions, check out our tutorial video below.

About the Budget Game

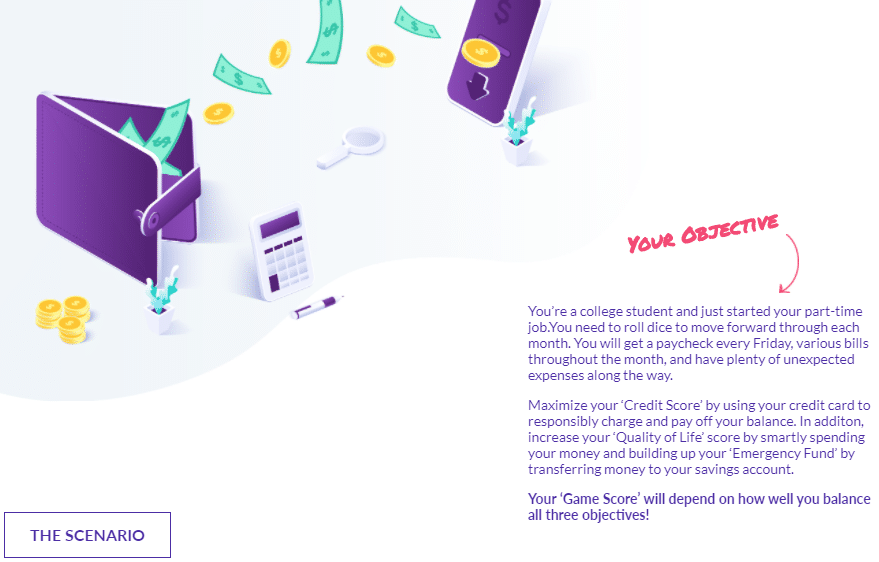

- Your students take on the role of a college student with a part-time job – in most scenarios, students have roommates, so they need to manage shared household expenses for the first part of the game.

- They graduate from school and become a full-time worker part-way through the game – they become a full-time worker (40-hour work per week), with more consistent income, but also with bigger expenses, since they no longer have roommates.

- Emphasis is on managing CASH FLOW and reinforcing PAY YOURSELF FIRST saving strategy – the goal is not necessarily to make students break their expenses down on a spreadsheet. The idea is to make students control and manage their expenses and income to build healthy finance habits.

Students Objectives

- Emergency Fund – Students’ first major goal is to save an Emergency Fund of $1000 – doing so earns a huge point bonus

- Credit Score – Students have a credit card they can use for purchases. Using it responsibly builds up their Credit Score and increases their Credit Limit.

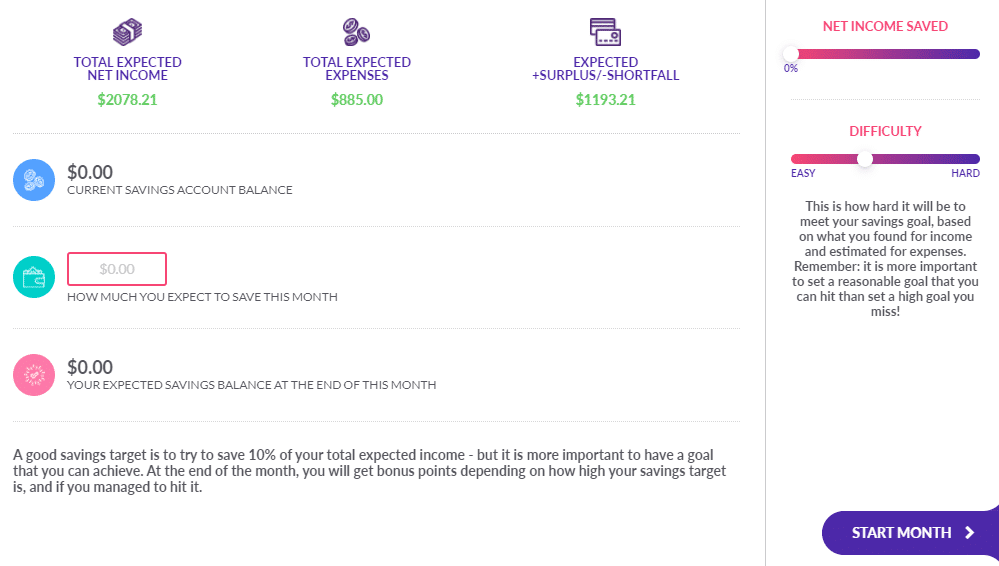

- Savings Goals – We ask students to set a “Savings Goal” every month. Students get bonus points if they save at least 10% of their income every month.

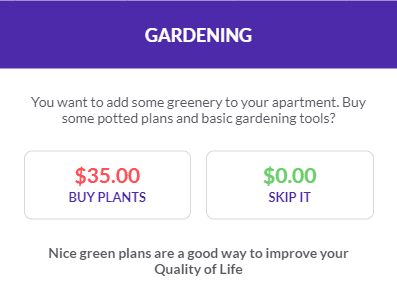

- Quality of Life – Avoiding every expense is not a winning strategy. Students earn “Quality of Life” points by buying nice things, having a better apartment, and spending time with friends

- “Life” Balance – Students also need to take care to spend time on chores or studying – their landlords give inspections and fines, and failing an exam can have big penalties.

Launching the Game

To kick off the game for your class, give them a prompt describing their scenario:

You are taking on the role of a college student in their last semester. You have a part-time job and are sharing an apartment with roommates. You will earn a paycheck each week, have bills to pay, and a credit card you can use – your goal is to build up your Emergency Fund and Credit Score while maintaining a high Quality Life.

After you graduate from school, you will move to a new apartment on your own and start your full-time job. You will have more (and bigger) bills, but also a bigger, steady paycheck. Keep hitting your Savings Goals and keep a high Credit Score and Quality of Life to max out your financial future!

– This is important because it helps students understand what they’re doing in the game as they’re moving through time. They need to understand that this transition from a student to a worker is very different –

First Learning Points – Unplanned Expenses

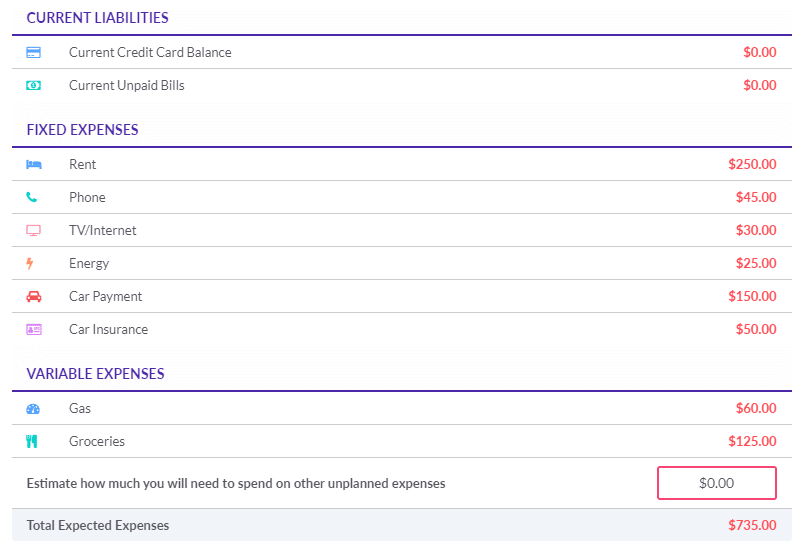

When students start the game, one of their first goals is to balance their expected income and expenses so they can set their first Savings Goal.

We give students most information, but they need to take a guess at how much they will spend on “Unplanned” expenses each month.

This is a key learning point – the first month will be a complete guess, but after a couple of months, students will see that small “impulse” and “last-minute” purchases add up quickly to be a major part of their spending!

First Learning Points – Pay Yourself First

Every month students also need to set their Monthly Savings Goal.

The secret is that we don’t care what their expected expenses are – to get the most points, students need to save at least 10% of their expected income.

This is a key tenant of the “Pay Yourself First” savings strategy, a foundation of the budget game.

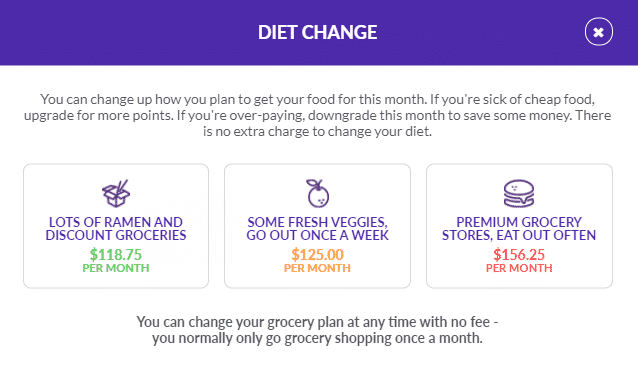

First Learning Points – Quality of Life

When students start the game, they are also asked to make several lifestyle choices:

- Where will they live? Crammed in with 5 roommates, or a nicer place with just 1 friend?

- What kind of TV/Internet package do they want? Just the basics, or a full-service package?

- How about their Cell Phone and data plan?

- And how will they be feeding themselves? Lots of cheap ramen and pasta, or lots of eating out?

These choices have a big impact on their Quality of Life – more expensive options give students a better Quality of Life and bonus points, but make it harder to hit their savings goals.

Discussion Point

Every student will have different events through the game – try launching a class discussion on what were the biggest expenses students faced each month. How frequently would students expect each expense to happen in the real world?

First Month

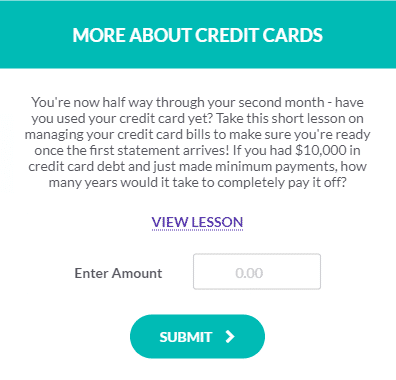

As students progress through the first few months, the game will pause and prompt students to complete short lessons.

We cover Credit and Debit, Savings Goals, Emergency Funds, and other essentials students need to succeed in the game in the first month, and more general finance concepts as the game goes on.

Life Events

At the end of each term, they get a life event. There’s two major types of led events: Fixed Expenses and Choices.

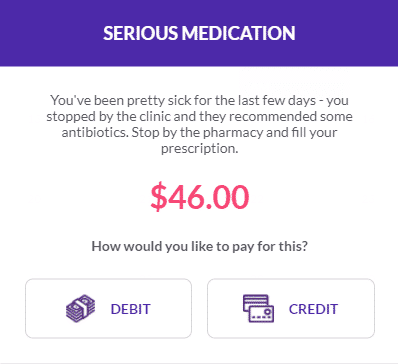

Fixed Expenses

Students don’t get any choice in it.

Either they need to choose to pay for something on their debit or credit card, either they need to choose to pay for it or skip it.

Choices

The choice cards have a big impact on their quality of life. Taking the more expensive option usually gives students a lot more points on the Quality of Life throughout the game.

Example: Students need to choose either they want or not to pay for house insurance. If they choose to don’t pay for it, there is a chance to have a break in every month, costing them several hundred dollars.

Discussion Point

Every choice in the budget game matters. The “Life Events” that pop up through the game are somewhat determined by the choices students make as they play.

What happened to you this month? What did you do before that had an impact on this? What would you have changed to make this outcome better? You can discuss this with students since they can give a recap of what worked well and what they would have changed in the past.

Ending the First Month

At the end of the first month, students get a summary of their savings and expenses, along with their progress to their savings goal.

Hitting a savings goal of 10% or more of their income earns big bonus points.

Teacher Tips

Make sure to play at least the first month of the game together as a class

End the first month of a recap – what were unexpected expenses? How did students cope? What will they do differently next month?

Assessments

Building assessments around the budget game is a matter of art. You will get the most out of your students if you ask them to provide “Monthly Summaries” as written document – specify what went right, wrong, and what they plan to do to fix it.

Be sure to also use the Assignments built into PFinLab — these have quizzes with automatically-graded quizzes you can use for more objective grading!

The Next Months…

Students will build up their Credit Score and Emergency Fund for the first part of the game, with lessons along the way.

Keep students “paced” by completing assignments and quizzes, rather than hour-long blocks of just the game itself.

Students will build up their Credit Score and Emergency Fund for the first part of the game, with lessons along the way.

Keep students “paced” by completing assignments and quizzes, rather than hour-long blocks of just the game itself.

The Rankings

The Budget Game also has a ranking page, showing student rankings by Overall Score, Net Worth, Credit Score, and Quality of Life.

Pay attention and give students shout-outs – even students at the bottom of the list!

Graduation

After playing as a part-time student for a semester, students “Graduate” from school and start their first full-time job.

They will need to pick a new place to live and other settings (as they no longer have roommates), and now get a consistent 40-hours per week salary at a higher pay grade.

Key Learning Point

The starting salary students get when starting their full-time job depends on how much they “studied” when a student. Students who “studied” often get a bigger paycheck with their full-time job!

Full-Time Mode Differences

- Bigger Bills – Students no longer have roommates, their bills all go up significantly

- Bigger Paychecks – Students have a pay raise and work a steady 40-hours a week

- Professional Development – Instead of studying, students can undertake “Professional Development” on the weekend (and raise their salary with enough of it)

- New Bills – New “Student Loan” and “Health Insurance” bills to pay every month

Key Learning Point

On the weekend, “Study” becomes “Professional Development” – as every student in the modern economy should understand the importance of lifetime learning. Conducting “Professional Development” frequently leads to a raise at their job!

Other Full-Time Mode Differences

Once students start their full-time job, they will be faced with even more choices and long-term impacts than before.

- Getting a pet? Expect to spend more at the grocery shop, and new vet bills pop up as Life Events… But also expect to boost your Quality of Life.

- More emphasis on household expenses, insurance, and general “Adulting”

Key Learning Point

As students complete 6, 12, 18+ months of the game, most of the healthy financial habits should become second nature.

After 12 months, how many students have a full 840 credit score? Launch a class discussion with both the students at the top and bottom of the class rankings to identify what went right and wrong, and discuss the importance of establishing healthy habits early!